Polymarket, the leading prediction market, announced that it will build its own L2. Is Polygon’s trump card gone?

Polymarket, the leading prediction market, announced that it will migrate from Polygon and launch an Ethereum Layer 2 network called POLY. Behind this "breakup" is a reflection of the reselection of the underlying network after the rise of the application layer, as well as the epitome of structural changes in the encryption industry.

(Previous summary: Betting on "OpenAI releases new model" on Polymarket, the market suspects the existence of insider arbitrage)

(Background supplement: Polymarket announced its return to the United States: approved by the CFTC to operate an intermediary trading platform as a "designated contract market")

Contents of this article

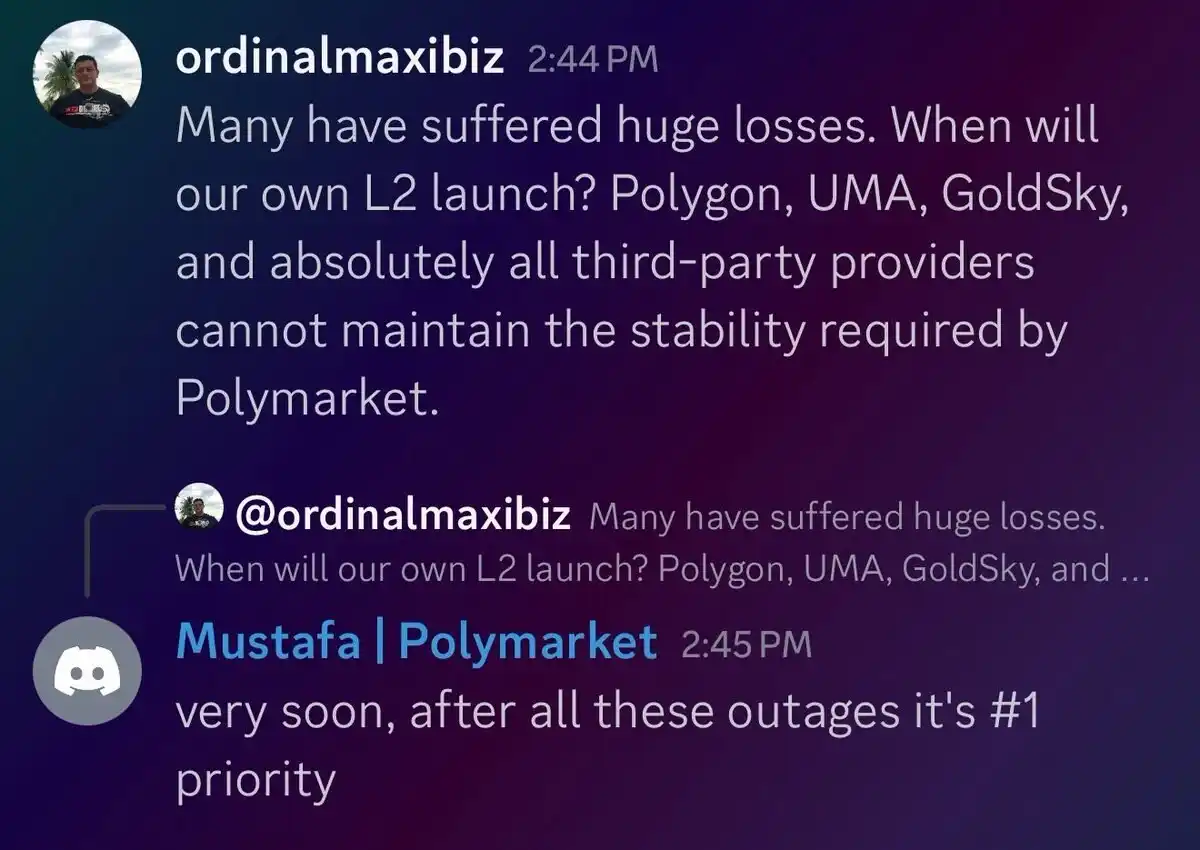

A news about the prediction market leader Polymarket has attracted widespread market attention: Polymarket team members Mustafa confirmed in the Discord community thatPolymarket plans to migrate from Polygon and launch an Ethereum Layer 2 network called POLY, which is the current priority of the project.

An unsurprising "breakup"

Polymarket chose to quit Polygon It’s not surprising. One is the application layer representative of the popular Fried Chicken, and the other is the old bottom layer that is declining. There is a mismatch in market popularity and value expectations between the two. As Polymarket gradually grows into a new behemoth, Polygon's unstable network performance (the latest failure occurred on December 18) and its relatively weak ecosystem have objectively constituted a limitation on the former.

For Polymarket, building its own portal means a win-win choice in both product and economic dimensions.

In terms of products,In addition to seeking a more stable operating environment, building a self-built Layer2 network can help Polymarket reversely customize the underlying features according to its platform requirements, thereby more flexibly adapting to future upgrades and iterations of the platform.

The more important significance is reflected in the economic level. Building a self-built network means that Polymarket can integrate the economic activities and surrounding services derived from its platform into its own system, preventing relevant value from spilling over to external networks, and gradually settling into its own systemic advantages.

Explicit and implicit economic contributions

As an application layer, the popularity of Polymarket once brought objective direct economic contributions to Polygon. The data history compiled by data analyst dash in Dune shows:

·Polymarket has 419,309 active users this month, and the total number of historical users is 1,766,193;

·The total number of transactions this month is 19.63 million transactions, and the total historical transaction volume is 115 million;

· The total transaction volume this month is 1.538 billion US dollars, and the historical total transaction volume is 14.3 billion US dollars.

As for how to evaluate Polymarket’s contribution to Polygon’s ecological economy, Odaily Planet Daily discovered a rather coincidental ratio when collating the data between the two.

· First of all, in terms of precipitated funds, Defillama data shows that the current total value of Polymarket’s entire platform position is approximately US$326 million, accounting for about a quarter of the total Polygon network lock-up value of US$1.19 billion;

· Secondly, there is the gas consumption situation. Coin Metrics reported last October that transactions related to Polymarket are expected to consume 25% of the entire Polygon network. gas;

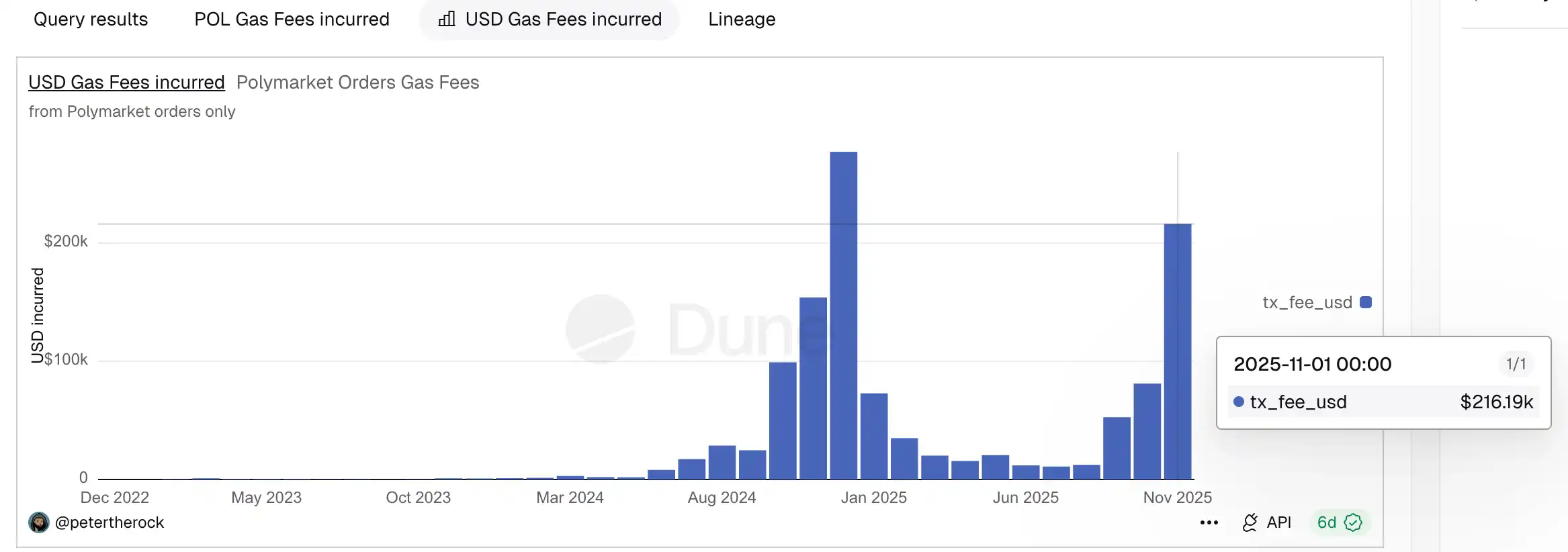

· Considering that the data is relatively long-term, we checked the recent changes. Statistics drawn by data analyst petertherock in Dune showed that Polymarket-related transactions consumed a total of approximately US$216,000 in gas in November, while Token Terminal statistics showed that the total gas consumption of the entire Polygon network that month was approximately US$939,000, which is also close to a quarter (approximately 23%).

Although there may be coincidences caused by statistical caliber and time window, similar results across dimensions can also be used as a reference to estimate the economic significance of Polymarket to Polygon to a certain extent.

In addition to quantifiable indicators such as active users, accumulated funds, transaction flow, gas contribution, etc.,Polymarket's impact on Polygon The economic significance is also reflected in a series of implicit contributions that are more difficult to measure directly, but are equally real.

The first is to revitalize the liquidity of stablecoins. All transactions in Polymarket are settled in USDC, and its high-frequency and continuous trading behavior has objectively significantly increased the circulation demand and usage scenarios of USDC on the Polygon network; The second is the incidental behavioral value of retained users. In addition to the prediction market itself, these users may also turn to other products such as DeFi on the Polygon ecosystem out of convenience, thereby increasing the overall ecological value of the Polygon network. Quantifying these contributions with very specific data constitutes the "real demand" that is most valued and scarce in the underlying network.

Why now? The answer is not difficult to guess

In fact, just from the perspective of user scale, data performance and market volume, Polymarket has the confidence to stand on its own. This is no longer a question of "should we leave?" but a question of "when to leave."

The core reason for choosing to start the migration at this point in time may be that the Polymarket TGE is approaching. On the one hand, once Polymarket completes the issuance of coins, its governance structure, incentive system and economic model will be relatively solidified, and the cost and complexity of subsequent underlying migration will increase significantly. On the other hand, the upgrade from "single application" to a "application + underlying" full-stack system itself means a change in valuation logic. Self-built Layer2 will undoubtedly open a higher ceiling for Polymarket at the narrative and capital levels.

All in all, Polymarket’s departure from Polygon is essentially not just a simple underlying migration, but a microcosm of the structural changes in the encryption industry. When top-level applications begin to have the ability to independently carry users, traffic and economic activities, if the underlying network cannot provide additional value, it will inevitably be "backstabbed".

Nothing but profit.